Picks for '26

Apologies for the long wait…been doing a lot of research lately and wanted to have everything teed up for this article. Let’s get into it.

Quick Macro Update

GDP is red hot at 4-5% with many saying it could go higher and the Fed is cutting rates.

The tax cuts from the Big Beautiful Bill are about to have an impact on people’s tax returns (more refunds).

Possible stimulus checks?

Trump is directing the government to purchase mortgage bonds in effort to bring down mortgage rates.

Trump is looking to increase military spending to $1.5T.

The economy is hot. This is the plan of the Trump Administration: intervene where needed and rapidly expand growth.

This will undoubtedly result in inflationary pressures down the road.

You need to own assets.

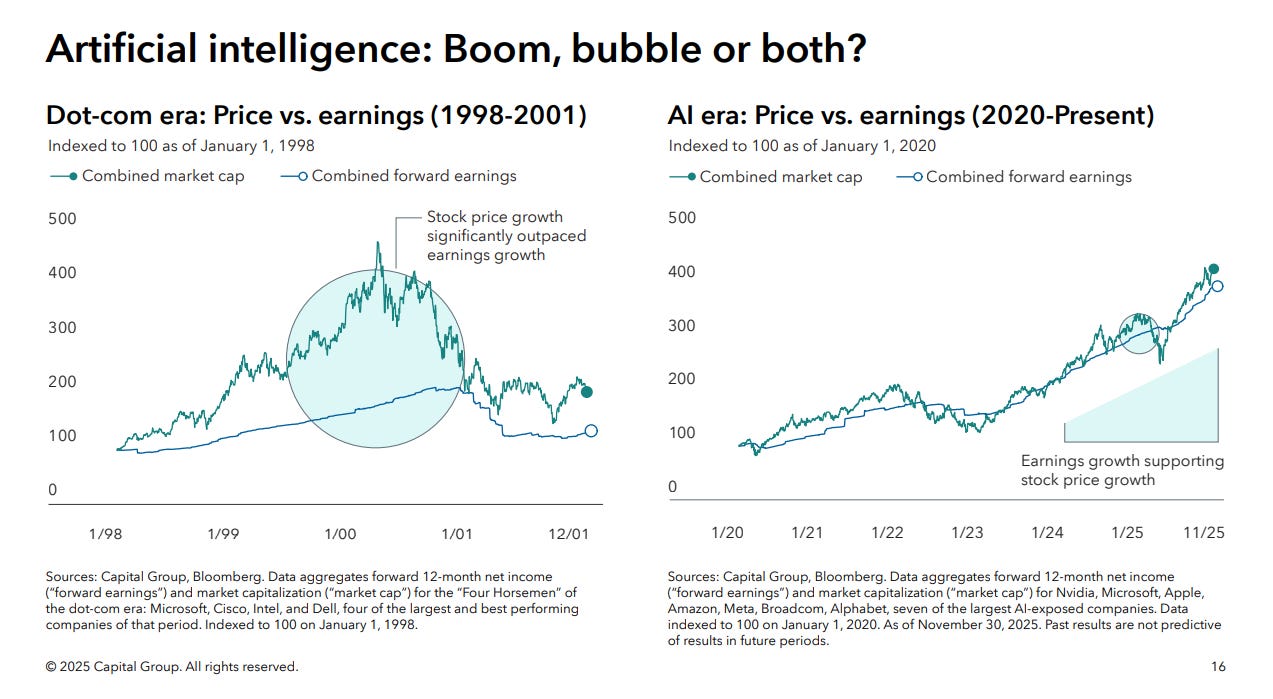

Is It A Bubble YET?

No.

Just because something goes up significantly in price doesn’t mean it’s in a bubble. Companies can rerate.

Here’s a look at the market caps of stocks charted against their forecasted earnings. Dot-com era vs right now.

Prices are inline with forward earnings.

What’s In For This Year

The AI trade isn’t over. It’s shifting.

I’ve written about this recently but I want to really hone on this thesis.

We’ve spent the last two years obsessing over software — chatbots, LLMs, SaaS AI plays. That was Phase 1.

Phase 2 is about the physical stuff. The atoms. The infrastructure that actually makes AI work in the real world. You’re already seeing this play out if you’re paying attention.

Power plants. Copper wires. Memory chips. Cooling systems. Grid infrastructure.

This is where the money flows next.

AI is moving from answering questions to doing things. Autonomous vehicles. Humanoid robots. Data centers that consume entire power grids.

Whereas before, the bottleneck was GPUs. We couldn’t manufacture enough chips to meet the demand. Now, it’s power. It’s cooling. It’s land.

It’s the physical infrastructure.

This point made by Julien Bittel (@BittelJulien on X) is an important one:

Copper deficit projected at 10 million metric tons by 2040. New mines take 20-30 years to develop. Data center power demand is outpacing generation capacity.

These aren’t financial problems you can print away.

The setup for 2026: abundant liquidity chasing scarce physical assets.

Pix For Twenty-Six

These are the names I’m watching/scaling into.

Micron (MU) — The Memory Monopolist

The idea is simple: HBM (High-Bandwidth Memory) is the single most supply-constrained component in AI infrastructure.

Micron owns 25% of the HBM market. Sold out through 2028.

Yes, the stock has run 250%+ in the last year. But you’re still paying ~10x forward earnings for 200% EPS growth. The PEG ratio of 0.15-0.19 is absurd. You’re getting growth almost for free.

It hit an ATH of $412 last week. Is it extended? Yes. Does the fundamental story still hold? Absolutely.

Entry strategy: Don’t chase at ATH. Wait for pullback to $340-360 range (10-15% off highs). Scale in: 1/3 on first pullback, 1/3 on 15% pullback, 1/3 on 20% pullback. Patience here.

This is the highest-conviction name on the list.

Vertiv (VRT) — The Cooling Kingpin

Vertiv sells the entire ecosystem of power and cooling for AI data centers.

Their edge? Deep integration with Nvidia. When Nvidia designs a new reference architecture, Vertiv co-engineers the cooling infrastructure.

The 2026 catalyst: Liquid-to-chip cooling becomes standard. Nvidia’s Blackwell and Rubin platforms force new builds to adopt liquid cooling. Vertiv commands higher margins on these systems.

Risk: Valuation is elevated. Wait for pullback to $160-170 for better entry.

Copper (COPX / FCX) — The AI Enabler

Every data center requires massive copper infrastructure. Wiring, cooling, power transmission.

Supply deficit projected at 150,000 tonnes in 2026. Expanding to 10 million tonnes by 2040.

New mines take 20-30 years to develop. This is structural scarcity.

Vehicle choice: COPX for diversified exposure (41 miners). FCX for concentrated conviction in Freeport-McMoRan.

COPX has run to ~$88 — extended from where I’d prefer to buy. Wait for 10-15% pullback to $75-80 range for better entry.

Iris Energy (IREN) — The Power Moat

I’ve written about IREN before. The thesis is simple.

IREN secured 3GW of grid-connected power when it was cheap. Capacity competitors cannot replicate. Microsoft’s $9.7B, 5-year contract validates the model.

At $6.8M/MW, IREN trades at a discount to what hyperscalers pay to build equivalent capacity ($15-20M/MW).

Catalyst: Second hyperscaler deal (60-70% probability in 2026).

Risk: Execution. Speculative position sizing only. Wait for a pullback after it’s recent runup.

Pairs well with DGXX which I’ve discussed in previous articles. Both are picks-and-shovels plays on the next AI investment leg.

What’s Out?

Let’s talk about the elephant in the room.

Software stocks are facing an existential threat. And most investors haven’t figured it out yet.

The thesis is simple: AI doesn’t just help software companies. It replaces them.

Think about what most SaaS businesses actually do. They automate workflows. They organize data. They help teams collaborate. They generate reports.

What does AI do? The same thing. Faster. Cheaper. Without the $50/seat/month subscription.

Software companies have traded at insane multiples for a decade because of one thing: gross margins.

80%+ gross margins. Recurring revenue. Land and expand. The playbook was beautiful.

But here’s what’s happening now.

AI tools are commoditizing features that used to cost thousands per year. A $15/month ChatGPT subscription can now do what entire software categories were built to do.

Microsoft, Google, Amazon — they’re not just building AI. They’re bundling it into everything.

Microsoft 365 Copilot. Google Workspace AI. AWS Bedrock.

If you’re a mid-tier SaaS company, you’re now competing against features that come free with enterprise subscriptions your customers are already paying for.

That’s not competition. That’s extinction.

Many of these names have been beaten up pretty badly so you may see a bounce, but for a long-term investor, I’d be very cautious.

GENCO